Indiana's Rural and Urban Housing Issues

Hint: They aren't what you think

Note: This is an extract from our Rural Indiana study. It’s findings are likely relevant to any rural place in the Midwest. It builds on work done previously, updating the data on home profitability.

In examining the housing sector in Indiana’s rural and urban counties, our goal is to better understand the size and condition of housing markets across the state. We use data from the US Census Bureau and the Federal Housing Finance Authority. These data are more accurate sources of data on the quantity and price changes of housing than are Multiple Listing Services (MLS), which only includes homes that pass through realty companies for sale, excluding a significant source of housing supply and prices.

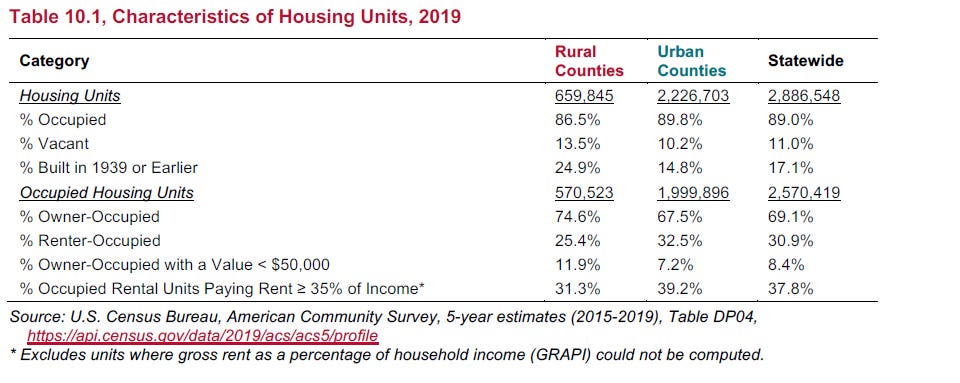

The US Census Bureau’s American Community Survey estimates that there are over 2,886,500 housing units in the state as of 2019. Of these units just over 316,100 (11%) are vacant (Table 10.1). While there is a lot of variation in vacancy rates between Indiana counties, ranging from 4.4 percent in Hendricks County to 31 percent in Crawford County (Table A.1), Table 10.1 shows that vacancy rates are generally higher in rural areas (13.5%) and the housing stock is older, with almost a quarter (24.9%) built more than 80 years ago. A larger share of housing units in rural areas are owner occupied (74.6%), and not surprisingly home values in rural areas tend to be lower compared to urban areas, with just under 12 percent having a value less than $50,000 compared to 7.2 percent in urban areas.

On the flip side, the share of housing that is renter occupied is lower in rural areas (25.4%) compared to urban areas (32.5%), and fewer renters pay more than 35 percent of their income on rent in rural versus urban places (31.3 percent vs 39.2 percent, respectively). Across the state, this statistic ranges from 16 percent of renters that pay more than 35 percent of household income in Steuben County to 51.1 percent in Monroe County.

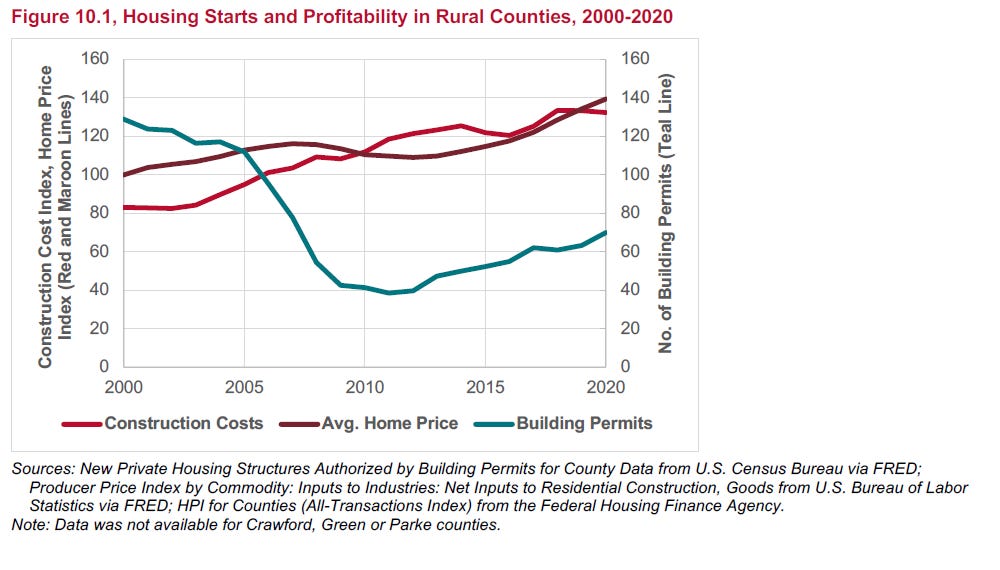

Next, we examine factors affecting the profitability of speculative home construction in rural and urban counties, updating the work of Hicks and Faulk (2019). By “speculative home construction” we mean new homes constructed by a builder before a buyer is found. In figure 10.1 below, the blue line is a national measure of construction costs and includes a 17 percent builder profit (Glaser and Gyourko 2005, 2018), the orange line represents home prices averaged over rural counties in the state, and the gray line represents the average number of building permits issued in rural counties for each year between 2000 and 2020. This figure clearly shows that before 2010, the average home price in rural counties was higher than the cost of construction. From 2010-2019, construction costs were higher than average home prices although from 2016 to 2018, they were very close. During 2020, average home prices were higher than construction costs, and the number of building permits were low. This matters because builders are generally unwilling to engage in speculative construction unless the price of housing is higher than the construction costs.

The underlying data shows variation in this relationship among rural counties. Several counties (including Adams, Blackford, Cass, Fayette, Grant, Henry, Huntington, Miami, Randolph, Tipton and Wayne) had not reached profitability by 2020. Data on Crawford, Parke and Greene Counties were not available to calculate this profitability measure.

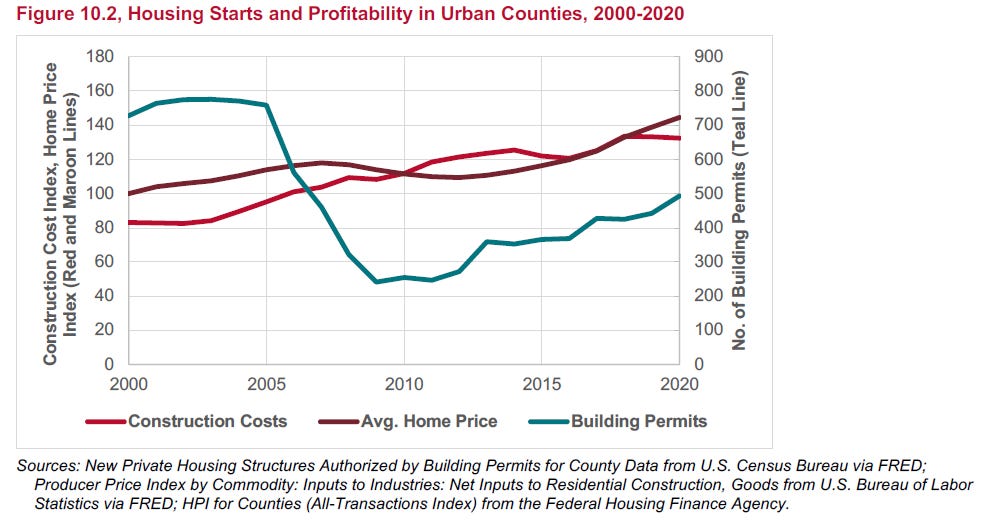

Figure 10.2 shows a similar graph for Indiana’s urban counties. Average home prices were higher than construction costs before 2010. After 2010 and until 2018, speculative building was unlikely to occur because construction costs were higher than or too close to the average price builders would be able to charge for new housing. After 2018, building was profitable again, and there was a uptick in the number of building permits issued. The urban counties that had not reached profitability by 2020 were Delaware, Howard, Madison, Union, and Vigo.

As in most places, the Great Recession reduced both housing prices and new home construction in Indiana. However, the cost of constructing a new home has continued to rise, making speculative new home construction unprofitable across much of Indiana until very recently. As of 2020, speculative new home construction is clearly profitable in 71 of 92 counties (32 rural and 39 urban). In several of these counties, it only became profitable during 2020. In 18 of 92 counties (13 rural and 5 urban), it was still not profitable to construct new speculative homes as of 2020. In the remaining three counties (rural), the data was not available make a determination. While price increases during the pandemic has served as an incentive to construct more housing, supply side issues such as labor shortages in the construction industry and higher prices for construction materials are likely to stifle development in many parts of the state.

An important addition to this discussion is the role that population decline plays in the risk of an excess supply of housing stock. Housing is a durable capital stock, as table 10.1 illustrates. Statewide, more than one out of every 6 homes was built before the Second World War, and in rural places, nearly one in four homes were built before the war. As Glaeser and Gyourko (2006) describe, population decline leaves an excess supply of housing and causes a strong negative shock to local home prices. The resulting oversupply of vacant homes suppresses home values in counties, regions, and neighborhoods where they are most concentrated. This in turn attracts lower skilled workers to communities with more affordable housing.

Housing markets respond quickly and effectively to changes in supply and demand. Indeed, they are among the most responsive markets for physical goods. Many policymakers in Indiana believe their community faces a housing shortage, which should prompt government intervention. However, this is not typically true. More commonly, home prices and supply of housing are dampened by the market forces outlined above. So, in most places where new housing stock has not been added in recent years, the problem is not a shortage, but an oversupply of homes, which reduces market value of existing homes and new speculative construction. Subsidizing new housing will simply worsen this problem.

Recent market conditions have improved across much of Indiana, and as we write this there is a possibility that new home building in the wake of COVID will add higher quality housing stock to many counties. Still, where speculative building is not occurring, the most common problem is that the community’s actual demand for housing is so low relative to supply that building new homes is not profitable. That is not a failure of markets, but the result of housing markets responding to population decline and the resulting blight associated with the homes they vacate.