Flaccid epistemology: the weak connection between state and local taxes and economic growth

One of the more enduringly perplexing matters I encounter is the widespread belief that state and local tax rates play a large role in economic growth. This is a matter that has occupied the attention of economists since at least Adam Smith, and continues to generate significant analysis. But, legislative decisions to alter tax rates in order to promote economic growth are disconnected from what economists know about the relationship.

At the same time, legislators who wish to collect higher tax revenues ignore what we do know about which taxes tend to be most distortionary. Most acutely, they seem to misunderstand the incidence of taxes (or who actually pays them). This is not universally true of course, but the debate on corporate taxes provides the best example.

Corporate taxes are poplar on the left, despite the fact that corporations are owned by people who already pay income taxes. So, corporate taxes involve a double taxation of income earned from business. Importantly, the owners of these corporations are mostly retirement funds not wealthy individual investors.

Types of taxation and their incidence are complicated matters, and there are different types of expertise applied to taxation. A tax attorney will be very familiar with the legalities of each tax, but often shockingly ignorant of the incidence of taxes. I once faced down a tax attorney who was convinced businesses didn’t pay any sales tax because that was expressly illegal.

Economists aren’t trained in the law or accounting, so are equally ignorant in these domains (or at least this economist suffers that challenge). It is just helpful to be self-aware of these matters.

To deal with the complexity and incidence of taxes, economists have some rules of thumb that help define what a tax system ought to do or not do. The first of these is the mantra of “large base, low rate.” This means that most economic activity should be taxed, and by doing so will insure the rate of tax on each activity will be low. This helps achieve five the the major rules of thumb about taxes.

Taxes should be non-distortionary, or alter certain types of economic activity to avoid the tax

They should be equitable across levels of income, so that taxpayers with higher incomes pay a higher tax rate than lower income taxpayers.

Taxes should be equitable between types of activities, so that a dollar earned by one type of business is taxed in the same way a dollar earned in another line of business.

Taxes should be readily enforceable, so that they are easy to understand and that there are low compliance costs (by taxpayers) along with low administrative costs (by tax collectors).

Taxes should be transparent and easy to understand and support. This links the tax to the benefits it produces.

Taxes may also be adjusted to correct for market failure (e.g. higher taxes on cigarettes to dissuade smoking).

Obviously, there is a tension between these goals, but they provide a clear way to think about taxes. Underlying all this is a recognition that the real purpose for taxes is to fund government activities, which themselves do (or at least should) generate benefits for taxpayers. This clearly implies a trade-off between tax revenues and the quality of public services. Of course, this is issue is often lost in the midst of debate about the role of tax cuts and economic growth.

Over the past few decades there have been three important reviews of the research in this area. the one most economists point to is by Michael Wasylenko in 1997. This review was very influential. My favorite quote is this:

“When the business climate of a state becomes so problematic that tax laws need to be changed routinely to attract businesses, the practice may be a symptom of problems with the tax system itself and a signal that systematic tax reform might be a more useful approach.” Wasylenko, pg. 49

This study did find that tax rates mattered in the size of economic activity, but that it had a very modest effect. A second, very large and comprehensive review by Dan Rickman and Hongbo Wang was done in 2018. Their findings from a review of dozens of microeconometric studies are pretty clearly summarized as:

“We can conclude that state and local tax fiscal policy is not predictably a major driver of economic growth in the U.S., particularly in more recent decades. There does not appear to be any economic benefit from deviating greatly from other states in the structure of state and local fiscal policy” Rickman and Wang, pg. 27

I particularly commend this study since it is written both by regional economists, who think more about regional growth than taxes, and because it has 10 pages of table summaries of studies. I also like it because it reinforces a point that I frequently make that recent changes to the economy (mix of jobs, mix of household consumption) lessens the sensitivity of businesses a to tax differences. Conversely, this makes businesses and households far more sensitive to differences in the quality of local public services — which are significant determinants of quality of life.

Andrew Hansen has a very recent (2021) review of taxes and economic development that develops a great deal of discussion on individual tax instruments. This is especially useful in making clear that there is no panacea on eliminating individual taxes, such as income or property. I like his take on TIF, which remains the go-to economic development tool of so many

“The empirical literature that exists on the economic development effects of Tax Increment Financing (TIF) broadly points toward a conclusion that it is not an effective economic redevelopment tool.” Hansen, pg. 23.

What should be apparent is that thinking through the role of fiscal policy requires attending to both the spending and the collecting of tax revenues. Likewise, estimating the effect of tax rates on economic growth requires new empirical analysis.

The types of studies I mean are those like this one from Ojede, Atems and Yamarik that evaluate spending differences and how they influence growth. I also admire the work Tim Bartik continues to provide on the mechanics of tax incentives. There is also a lot of think tank work that should help keep policymakers more honest, such as this one from CBPP. Dagney Faulk and I have done work on Tax Increment Financing, the cost of government, and quality of services focusing mostly on Indiana. These state specific studies are too infrequently published, but are particularly relevant in their ability to isolate idiosyncratic features of state tax systems.

I don’t expect enough policymakers will read through the 120 odd pages in the three big reviews, which is a pity. Almost nothing government undertakes is done with more ignorance than change tax rates with the goal of stimulating economic growth.

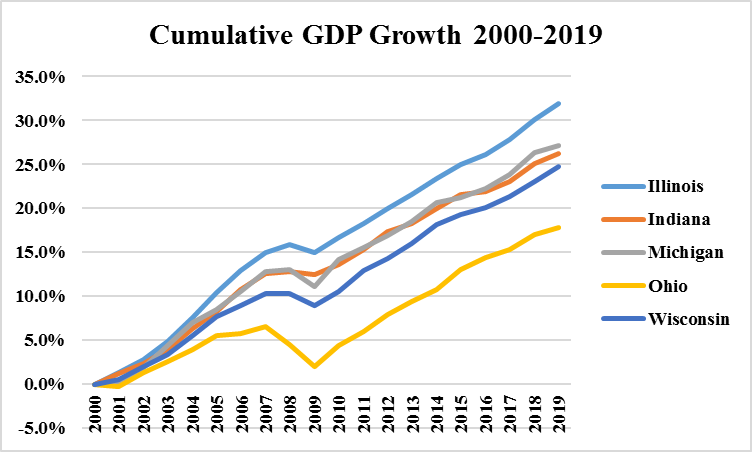

But, maybe the best way to deal with this is through the direct application of some really basic data. I start with cumulative GDP growth so far this century in the five Midwestern Great Lakes states.

Indiana is decidedly “middle of the pack” here. Obviously, a great deal of the interstate differences revolve around how well states worked through the Great Recession. Still Indiana has done much worse than that perennial policy scapegoat, Illinois, and not quite as well as Michigan, which had the worst decade of any state since the Civil War in population loss.

Have tax rates played a role in this?

Yeah, maybe so, but be honest with yourself. Which side would you prefer in the Oxford debate? That’s right, you’d much prefer to make the argument against that proposition.

The Indiana GOP provides a nice graphic of the state’s tax history. The most recent tax cuts will usher in annual cuts for the next seven years, providing ample opportunity to tout the low tax environment of the state. But, the two figures above show no link between business taxes and GDP growth. The high tax state had the best GDP growth, and the low tax state was only in the middle of growth.

Gross Domestic Product (GDP) is not the only measure of economic, jobs are also of keen interest by policymakers. Likewise, business taxes are not the only taxes that matter. In the graphs that follow, I try to connect the dot between taxes, quality of life and employment growth.

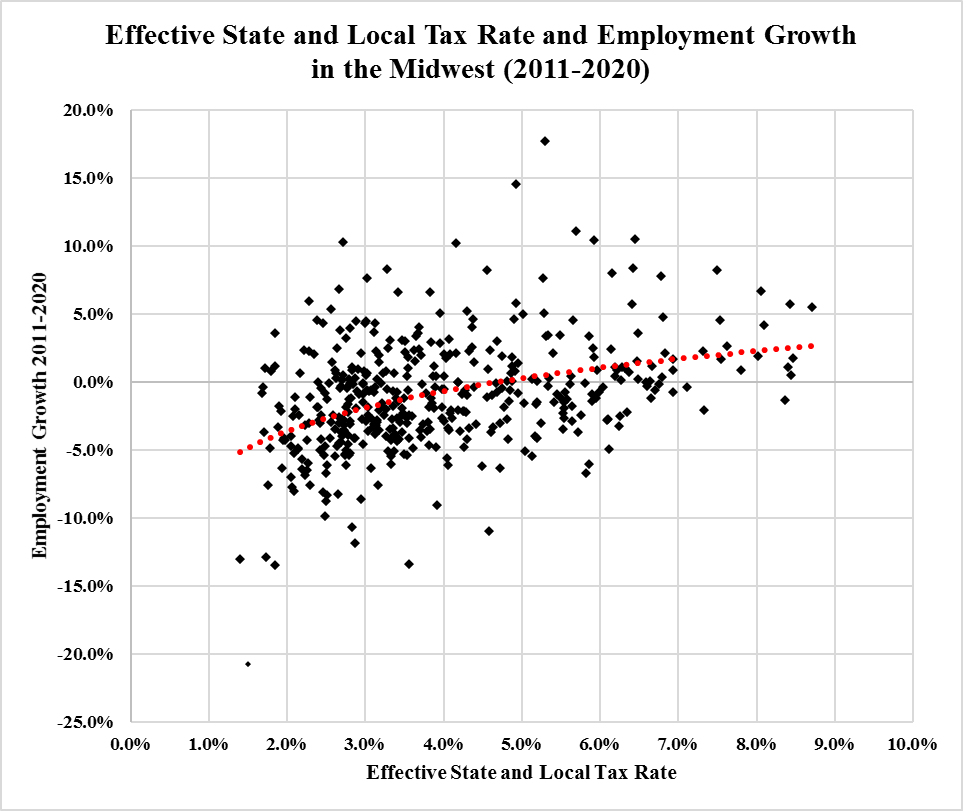

The employment data are, like the GDP data above from the Bureau of Economic Analysis. I use the same five states for comparison, but focus on county data. The effective tax data come from IRS county level records, in which the reported state and local taxes are a function of Adjusted Gross Income. The quality of life measures come from our Brookings study of quality of life.

So, first, a simple correlation. Are jobs moving to places with high or low state and local tax rates?

Employment growth in Illinois, Indiana, Michigan, Ohio and Wisconsin counties are positively correlated with effective state and local tax rates. Assuming that households and businesses are rational, they will, ceteris paribus, prefer to live in places with lower taxes. But, because they are rational, they will weigh other factors as well.

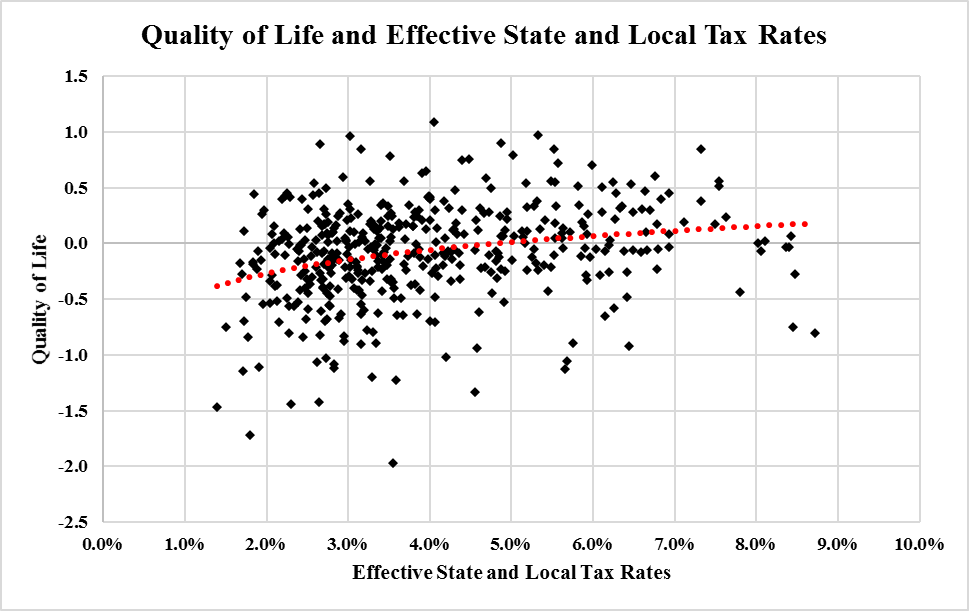

The Brookings study I cite above makes clear that both households and businesses care about the quality of local schools, local crime rate and blight, the opportunities locally for recreation and the arts, food stores and broadband. These are all things that government policy has a role in either promoting or dissuading. Particularly, with respect to the big budget items of state and local government: schools, health and public safety.

The question of relevance is whether there is a connection between these quality of life measures and state and local tax rates. I don’t find this too surprising, but there it is . . .

Now, let us go full circle and see whether or not that quality of life actually influences job growth. And, as we said in the Brookings Metro study, yes it does . . .

This snippet of evidence drawn from Midwestern states and counties makes a plain and convincing case that tinkering with tax rates will have no positive effect on economic development outcomes, or at least has not had such effects.

That should not be surprising. The bulk of research over the past two decades has come to the same conclusion. Is the case for tax cuts generating economic growth a closed matter? No, it isn’t. In some future date households and businesses might worry more about the price of public services and less about quality. But, that date is likely a long way away.

There is some pretty unambiguous guidance however, that will be clear to anyone who reads the tax review studies I’ve linked to in this essay. That is the simple observation that there are diminishing returns to both tax cuts and some public services. This is particularly true with respect to business and household location.

If you are a policymaker in a high tax state, cutting taxes might generate more economic benefit than the loss of public services they necessarily entail. The reverse is true for low tax states. Raising taxes in a low tax state will slow economic activity less than the economic growth generated by better quality public services.

Indiana is a state with very low taxes, and as a result, low levels and quality of public services. The tax cuts that are coming will both reduce our tax rates and the quality of public services. There may be reasonable justifications for cutting taxes, but growing the states economy is not among them.